Every year on March 8, the world celebrates International Women’s Day—a time to recognize the achievements of women, reflect on progress toward equality, and highlight the important role women play in business and leadership.

At TNT Accounting Services, this day has special meaning. As a woman-led accounting and bookkeeping firm, we understand the determination, resilience, and passion that women bring to entrepreneurship and professional services.

The Growing Impact of Women in Business

Women entrepreneurs continue to shape the modern economy. Across industries, women are starting businesses, leading organizations, and creating opportunities within their communities.

Small businesses owned and operated by women are growing rapidly in Canada, contributing to job creation, innovation, and stronger local economies. Many of these entrepreneurs are balancing multiple responsibilities while building sustainable businesses.

At TNT Accounting Services, we are proud to support women-owned businesses, freelancers, and professionals by helping them stay organized, confident, and prepared financially.

Financial Confidence is Key to Business Success

One of the most important foundations of any successful business is clear financial management. Having the right bookkeeping systems and tax planning strategies in place helps business owners make informed decisions and plan for growth.

Our team works with clients to simplify the financial side of running a business by helping with:

Small business bookkeeping

Tax preparation and planning

Financial organization and reporting

Cash flow awareness and budgeting

Preparing for tax season with confidence

By making finances easier to understand, we help business owners focus on what they do best—growing their businesses.

Supporting the Next Generation of Women Entrepreneurs

International Women’s Day is not only about celebrating achievements, but also about encouraging and supporting the next generation of women in business.

Access to financial education, mentorship, and reliable professional support can make a significant difference for new entrepreneurs. As a woman-led firm, TNT Accounting Services believes in helping business owners build the knowledge and confidence they need to succeed.

Celebrating the Women in Our Community

Today we celebrate the women who inspire us every day—our clients, partners, colleagues, and community members who are building businesses, supporting families, and strengthening the local economy.

From everyone at TNT Accounting Services, Happy International Women’s Day.

Need Help With Your Business Finances?

If you are starting a business, managing a growing company, or preparing for tax season, TNT Accounting Services is here to help.

People wait until the last minute to file their taxes… and then stress sets in.

But here’s the simple truth: the earlier you file, the earlier you receive your refund.

If you’re expecting money back this year, there’s no reason to let it sit with the government longer than necessary.

Why Filing Early Makes a Difference

When you file your tax return early:

1. You Get Your Refund Sooner

The Canada Revenue Agency (CRA) typically processes electronically filed returns in as little as two weeks. That means filing in February or early March could put your refund in your bank account weeks — even months — before the April rush.

Why wait until spring if you could have that money working for you now?

2. You Reduce Stress

Waiting until the deadline creates unnecessary pressure. Filing early gives you peace of mind and removes one major item from your to-do list.

3. You Avoid Delays

As we get closer to the April 30 deadline, processing times can slow down. Filing early helps you avoid the backlog.

4. You Protect Yourself from Fraud

Filing early also reduces the risk of tax-related identity theft. Once your return is submitted, no one else can file using your information.

“But I’m Missing a Slip…”

Many people delay filing because they’re unsure whether all their slips have arrived. In most cases, slips are available in your CRA My Account, and we can help confirm what’s still outstanding.

Don’t let uncertainty delay your refund.

Make Your Money Work Sooner

Whether your refund is going toward:

Paying down debt

Investing

Home improvements

A family vacation

Or simply catching up on bills

Getting it earlier gives you more flexibility.

Let’s Get It Done

At TNT Books, we make the process simple, secure, and stress-free. The sooner you send in your documents, the sooner we can file — and the sooner you can get your refund.

The Canada Groceries and Essentials Benefit, will be indexed to inflation, and builds on the existing Goods and Services Tax (GST) Credit and provide $11.7 billion in additional support over six years by:

providing a one-time top-up payment to be paid as early as possible this spring and no later than June 2026 (subject to Royal Assent)—equal to a 50% increase in the annual 2025-26 value of the GST Credit. This would deliver $3.1 billion in immediate assistance to individuals and families who currently get the GST Credit.

increasing the value of the Canada Groceries and Essentials Benefit by 25% for five years starting in July 2026 (subject to Royal Assent). This increase would deliver $8.6 billion in additional support over the 2026-27 to 2030-31 period, including to 500,000 new individuals and families.

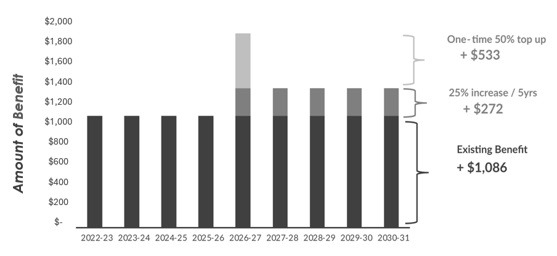

Canada Groceries and Essentials Benefit

Benefit amounts are illustrative, and do not reflect price indexation. Benefit years (July-June) are shown and top-up would be paid as early as possible in the spring of 2026 (no later than June, subject to Royal Assent).

Taken together, these measures would provide up to an additional $402 to a single individual without children, $527 to a couple, and $805 to a couple with two children. At these levels, Canada’s new government will be offsetting grocery cost increases beyond overall inflation since the pandemic.

After the one-time payment is made in the spring of 2026 (subject to Royal Assent), eligible families and individuals in Canada will receive the enriched regular payments under the Canada Groceries and Essentials Benefit as of July 2026 (subject to Royal Assent). The benefit will be paid quarterly, at the start of the quarter, to permit timely access to the funds to help families with day-to-day expenses. These amounts are additional to existing benefits such as the Canada Child Benefit, the Canada Disability Benefit, and the Guaranteed Income Supplement.

Under the proposed changes:

A single senior with $25,000 in net income would receive a one-time top-up of $267 plus a longer-term increase of $136 for the 2026-27 benefit year (total increase of $402). In total, they would receive $950 for the 2026-27 benefit year (including the top-up).

A couple with two children with $40,000 in net income would receive a one-time top-up of $533 plus an increase of $272 for the 2026-27 benefit year (total increase of $805). In total, they would receive $1,890 for the 2026-27 benefit year (including the top-up).

Table: Canada Groceries and Essentials Benefit, by family type*

Family Type

Maximum Base Amount for 2026-27

50% Top-Up

25% Increase to 2026-27 Amounts

Total Increase50% Top-Up + 2026-27 benefit year

Total Benefits Received 50% Top-Up + 2026-27 benefit year

(A)

(B)

(C)

(B) + (C) = (D)

(A) + (D)

Single

$543

+ $267

+$136

$402

$950

Couple, 2 kids

$1,086

+ $533

+ $272

$805

$1,890

*Assuming Royal Assent by March 31, 2026. Numbers may not add up to totals due to rounding. Example for a single individual assumes no children.

Enabling legislation for the proposed one-time top-up and further five-year increase to the Canada Groceries and Essentials Benefit will be tabled in the coming weeks. The proposed one-time top-up amount would be paid to all current recipients as a one-time, lump-sum payment as early as possible in the spring of 2026 (no later than June) based on eligibility to the GST Credit in January 2026, pending Parliamentary approval and Royal Assent of enabling legislation. The new Canada Groceries and Essentials Benefit would continue to be delivered quarterly in July, October, January and April.

Recipients would not need to apply for the additional payments, but should file their 2024 tax return if they have not done so already to be able to receive the top-up, and must file their 2025 tax return to receive the increased Canada Groceries and Essentials Benefit payments as of July 2026.

It is estimated that 12.6 million individuals and families would benefit from the new Canada Groceries and Essentials Benefit, representing a material support to Canadians that need it the most, while the government’s plan to build the strongest economy in the G7 takes effect.

If you receive federal benefits, including some provincial/territorial benefits, you will receive payment on these dates. If you set up direct deposit, payments will be deposited in your account on these dates.

Canada Pension Plan Includes the Canada Pension Plan (CPP) retirement pension and disability, children’s and survivor benefits.

Old Age Security Includes Old Age Security pension, Guaranteed Income Supplement, Allowance and Allowance for the Survivor.

Ontario Trillium Benefit (OTB) Includes Ontario energy and property tax credit (OEPTC), Northern Ontario energy credit (NOEC) and Ontario sales tax credit (OSTC).

Provincial and territorial tax rates vary across Canada; however, your provincial or territorial income tax (except Quebec) is calculated in the same way as your federal income tax.

Fraudsters are getting more sophisticated — and they often impersonate trusted institutions like your bank or the Canada Revenue Agency (CRA). These scams can look convincing, sound urgent, and arrive by email, text, phone call, or even mail.

At TNT Books, we regularly see clients receive suspicious messages and wonder: Is this real? Knowing the warning signs can help protect your money, your identity, and your peace of mind.

Below are key ways to recognize fraudulent requests and what to do if you receive one.

Common Red Flags to Watch For

1. Urgent or Threatening Language

Scammers rely on panic. Messages may claim:

Your account will be frozen

You owe back taxes immediately

Legal action or arrest is imminent

Benefits will be cancelled unless you act now

Legitimate banks and the CRA do not threaten arrest, demand immediate payment, or pressure you to act instantly.

2. Requests for Personal or Login Information

Fraudulent messages often ask for:

SIN numbers

Online banking usernames or passwords

One-time verification codes

Credit card details

Neither your bank nor the CRA will ask for sensitive information by email, text, or unsolicited phone calls.

3. Unusual Payment Requests

Be very cautious if you’re asked to pay:

By gift cards

By cryptocurrency

By wire transfer

Through e-transfer to a personal email address

The CRA does not accept these forms of payment.

4. Suspicious Links or Email Addresses

Watch for:

Misspelled sender names or domains

Links that don’t match official websites

Generic greetings like “Dear Customer” instead of your name

When in doubt, do not click. Go directly to the official website by typing it into your browser.

How the CRA Actually Communicates

The CRA typically contacts taxpayers by:

Mail (especially for formal notices)

Secure messages within your CRA My Account

Phone calls (but they will never demand immediate payment or threaten arrest)

If you’re unsure, log in to CRA My Account or call the CRA using the phone number listed on their official website — not the one provided in the message.

What to Do If You Receive a Suspicious Request

Pause. Don’t click, reply, or provide information.

Verify independently. Contact your bank or the CRA using official contact details.

Report the scam.

CRA scams: report to the CRA and the Canadian Anti-Fraud Centre

Banking scams: notify your financial institution immediately

Let your accountant know. Especially if the message relates to taxes, payroll, or business accounts.

Why This Matters for Small Businesses

Business owners are frequent targets because scammers know:

You manage multiple accounts

You deal with payroll and remittances

You may expect CRA communication

One wrong click can lead to financial loss or data breaches. Staying cautious is part of protecting your business.

Need a Second Opinion?

If you receive a message claiming to be from the CRA or your bank and aren’t sure if it’s legitimate, TNT Books is happy to help you assess it. A quick check can prevent a costly mistake.

Staying informed is one of the best defenses against fraud — and we’re here to help you stay protected.

As the year comes to a close, all of us at TNT Books would like to extend our heartfelt thanks to our clients, partners, and community.

This year brought growth, challenges, and new opportunities—and we’re truly grateful to have supported you along the way. Whether we helped keep your books organized, guided you through tax season, or provided clarity around your finances, it’s been a pleasure working with you.

The holiday season is a time to reflect, recharge, and prepare for what’s ahead. As you celebrate with family and friends, we hope you enjoy peace of mind knowing your bookkeeping and accounting needs are taken care of.

Looking Ahead to 2025 & Tax Season

The new year will be here before we know it—and early planning makes all the difference when it comes to tax time.

📌 The personal tax filing deadline is April 30, 2026, and we strongly encourage clients to reach out early for 2025 tax planning and preparation. Getting started sooner helps reduce stress, avoid last-minute surprises, and ensure accuracy.

👉 To learn more about our services and secure your spot for the upcoming tax season, visit: Plans & Pricing

As always, our commitment remains the same:

Accurate and reliable bookkeeping

Clear, actionable financial insights

Personalized support tailored to your needs

From all of us at TNT Books, we wish you a joyful holiday season, a successful New Year, and continued financial success in 2025 and beyond.

As the calendar year winds down, Canadians often shift their focus to holiday preparations—but it’s also one of the most important times to plan ahead for taxes. Whether you’re an individual taxpayer or a business owner, year-end is your last opportunity to take strategic steps that can reduce your tax burden and set you up for a strong start to the new year.

Below are the most effective year-end tax planning strategies for Canadians, along with practical tips you can implement before December 31.

For Individuals

1. Maximize Your RRSP & TFSA Contributions

While RRSP contributions can be made up until 60 days after year-end, contributing earlier allows you to take advantage of tax-deferred growth sooner. If you expect to be in a higher tax bracket this year than next, maximizing your RRSP can provide a more valuable deduction.

TFSA contributions aren’t tax-deductible, but all growth and withdrawals are tax-free—making it a smart vehicle for long-term savings. Confirm your remaining contribution room through CRA’s MyAccount.

2. Consider Tax-Loss Harvesting

If you hold non-registered investments that have declined in value, you can sell them before year-end to realize capital losses. These losses can offset capital gains realized this year or be carried back/forward to other tax years.

Be mindful of the superficial loss rules, which restrict claiming a loss if you repurchase the same security within 30 days.

3. Make Charitable Donations Before December 31

Eligible donations made before year-end can produce valuable non-refundable tax credits. Donations of publicly traded securities with accrued gains may offer additional tax advantages, including avoiding capital gains tax.

4. Take Advantage of Medical and Child-Care Expenses

If you’re close to meeting minimum thresholds for medical expense claims, consider advancing planned expenses into the current year. Child-care expenses—including day camps, daycare, and some tutoring—may also be deductible if paid before year-end.

5. Review Your Income Sources

If you have flexibility (e.g., self-employment income), consider whether deferring income into the next year may reduce your tax obligation—especially if you anticipate being in a lower tax bracket.

For Businesses

1. Review Capital Asset Purchases

Under Canada’s Capital Cost Allowance (CCA) rules, purchasing eligible equipment, vehicles, computers, and other capital assets before year-end may allow you to claim a portion of the depreciation this year. Certain assets may qualify for immediate expensing, depending on current CRA rules.

2. Optimize Owner Compensation

Many incorporated business owners should evaluate their salary vs. dividend mix prior to year-end. A salary can create RRSP room and allow for CPP contributions, while dividends may offer tax efficiency depending on provincial rates.

Reviewing this with an accountant ensures alignment with your income needs and long-term tax plan.

3. Manage Inventory and Write-Downs

Year-end inventory counts can identify obsolete or unsellable goods. Writing these down can reduce taxable income and provide a clearer financial picture heading into the next year.

4. Pay Employee Bonuses Before December 31

If the company declares bonuses before year-end—even if paid within 179 days—they’re deductible in the current fiscal year. This offers flexibility while still improving employee retention and motivation.

5. Review GST/HST and Payroll Accounts

Year-end is a good time to ensure your GST/HST filings, instalments, and payroll remittances are up to date. Errors or late payments can result in penalties that are easily avoidable with a cleanup before the year closes.

General Best Practices for Everyone

Stay Organized

Collect receipts, charitable donation slips, medical records, investment statements, and business documents. Digital recordkeeping tools can simplify your life come tax season.

Check CRA Updates

Tax credits, contribution limits, and rules often change from year to year. Reviewing current CRA guidance ensures your planning aligns with the latest regulations.

Consult a Professional

A tax advisor can help identify opportunities specific to your situation—particularly around compensation strategies, corporate structure, investment planning, and deductions you may not be aware of.

Final Thoughts

Year-end tax planning isn’t just about reducing your tax bill—it’s about making informed decisions that support your financial goals. By taking time now to review your income, investment

What Canadians need to know about new tax measures, credits, and policy changes — and how they could impact your finances.

After a months-long delay, the 2025 federal budget introduced a suite of tax measures that will shape the financial landscape for Canadians in the coming years. While some changes are incremental, others mark significant shifts in policy, with implications for individuals, business owners, and investors alike. Here’s a closer look at the most impactful changes and what they mean for Canadians based on insights from Jamie Golombek’s 2025 federal budget report (PDF, 455 KB)Opens a new window..

Middle-class tax cut: More money in Canadians’ pockets

A headline item is the reduction in the lowest personal income tax rate. Announced earlier in May and now included in Bill C-4, the first marginal personal income tax rate will drop from 15% to 14.5% for 2025, and to 14% in 2026 and beyond. The updated tax brackets and federal tax rates for 2025 are as follows:

Taxable income

Federal tax rate

Up to $57,375

14.5%

$57,375 – $114,750

20.5%

$114,750 – $177,882

26.0%

$177,882 – $253,414

29.0%

Above $253,414

33.0%

This move is intended to put more money in the pockets of Canadians, particularly those in lower and middle-income brackets. However, a technical quirk threatened to reduce the value of the tax savings of non-refundable tax credits since the value of those credits is also based on the lowest tax bracket. To address this, the government introduced a “Top-up tax credit” designed to ensure that no taxpayer is worse off due to the rate reduction — a targeted fix that will apply from 2025 to 2030.

Home accessibility and medical expense credits: No more “double-dipping”

The Home Accessibility Tax Credit (HATC) and the Medical Expense Tax Credit (METC) have long provided relief to seniors and individuals with disabilities undertaking certain home renovations. Under current rules, it was possible to claim both credits for the same expense. The budget closes this advantage, effective January 1, 2026, meaning that Canadians have until the end of 2025 to make claims under both credits for a single expense.

New support for personal support workers

Recognizing the essential role of personal support workers (PSWs), the budget introduces a temporary refundable tax credit for eligible PSWs working in health care establishments. The credit is worth 5% of eligible earnings, up to $1,100 annually, and will be available from 2026 to 2030. Notably, amounts earned in British Columbia, Newfoundland and Labrador, and the Northwest Territories are excluded, as these provinces have separate agreements in place to increase PSW wages.

Flow-through shares and critical minerals

Flow-through shares let corporations pass certain exploration and development expenses to investors, who can deduct these costs from their taxable income. The Critical Mineral Exploration Tax Credit (CMETC) gives investors a 30% tax credit on eligible mineral exploration expenses. The list of qualifying minerals is expanded in the 2025 budget to include bismuth, cesium, chromium, fluorspar, germanium, indium, manganese, molybdenum, niobium, tantalum, tin, and tungsten. This is designed to bolster Canada’s position in the global supply chain for clean technology and advanced manufacturing. These new rules apply to flow-through share agreements made after November 4, 2025 and before March 31, 2027. However, the budget cancels a previously proposed change that would have allowed full resource expense deductions under the Alternative Minimum Tax (AMT) regime, which may result in higher taxes for some investors.

Trust planning: Closing loopholes

The “21-year rule” prevents trusts from indefinitely deferring capital gains taxes by deeming a trust to have disposed of its property every 21 years. Although this disposition can be avoided by transferring the property at its cost to beneficiaries, if the transfer is to another trust the original 21-year period will continue to apply. The budget tightens anti-avoidance rules to capture indirect transfers of property between trusts — an area where tax planners have previously found workarounds. This change, effective for transfers after November 4, 2025, underscores the government’s intent to ensure fairness and limit aggressive tax planning.

Repeal of underused housing and luxury taxes

The Underused Housing Tax (UHT), which targeted underused and vacant homes generally owned by non-residents, will be eliminated for the 2025 calendar year and beyond. No UHT will be payable or returns required for 2025 and future years, though obligations for previous years remain. Similarly, the luxury tax on boats and airplanes, which applied to high-value purchases, will end after November 4, 2025. It will continue to apply to higher-end vehicles.

RRIF minimums: No change for retirees

Despite campaign promises, the budget does not reduce the required minimum withdrawals from Registered Retirement Income Funds (RRIFs). Many seniors had hoped for more flexibility to manage their retirement savings, but for now, the status quo remains.

Business tax measures: Support for manufacturing, cancellation of entrepreneur incentives

To spur investment in manufacturing, the budget introduces temporary immediate expensing for certain new or improved manufacturing and processing buildings. This allows qualifying businesses to deduct 100% of eligible capital costs in the first year, for properties first used before 2030. However, the previously announced Canadian Entrepreneurs’ Incentive, which would have lowered the tax rate on up to $2 million of capital gains from selling shares of a qualifying corporation over an individual’s lifetime, has been cancelled. The proposed enhanced $1.25 million lifetime capital gains exemption remains.

Administrative changes: Automatic filing and bare trust reporting

Our tax system relies on self-reporting, which means some low-income Canadians may miss out on income-tested government benefits simply because they don’t file a tax return. The budget proposes a solution: the CRA will be able to automatically file a tax return for eligible individuals whose income comes from sources already reported to the CRA, and who haven’t filed a return in the last three years. Before filing, the CRA will send the taxpayer the information it has, giving them 90 days to make changes or opt out. This could start as early as the 2026 tax season. Meanwhile, the requirement for bare trusts to file tax returns has been delayed until 2026, giving trustees some breathing room to prepare the returns.

What it all means

For Canadians, the 2025 federal budget delivers a combination of tax relief, targeted credits, and tighter rules designed to close loopholes and promote fairness. As always, those affected by the changes should consult a tax professional to understand the implications for their specific circumstances. To discuss how these changes may affect your own goals and financial plans, speak with a CIBC advisor for personalized advice and support.

Maximize your tax savings with strategic planning, charitable giving and professional advice before December 31.

As the end of the year approaches, it’s an ideal time to consider tax planning opportunities that could benefit you and your family. From charitable giving to optimizing registered plans, there are several smart moves you may be able to take advantage of before December 31. But as Jamie Golombek, Managing Director, Tax and Estate Planning, CIBC Private Wealth, points out, “You don’t have to do this alone. This stuff is complicated, and you should rely on professionals.” Whether you consult with an accountant, a lawyer, a tax advisor, or a financial advisor at CIBC, expert guidance can help you make the most of these opportunities.

Income splitting: Take advantage of lower prescribed rates

One strategy to consider is income splitting, which can help reduce your overall family tax burden, especially when rates are favourable. Golombek explains, “Maybe you’re going to set up what’s called the prescribed rate loan and loan money to a lower-income family member, or even to kids, using a family trust. Now that the prescribed rate has dropped to 3%, this is again a new opportunity that you might want to reconsider going forward, even to 2026.”

Turning losses into gains: Tax-loss selling

Another key year-end tip is tax-loss selling. “One of the most common things that we talk about before the end of every year is tax-loss selling, which is the opportunity to realize a capital loss that you might have in a non-registered portfolio and then use that loss to offset any other capital gains that you realized this year, or in the prior three years,” says Golombek. This strategy can offer a valuable refund if you’ve paid taxes on gains in the last three years.

Donate now, save Later

Charitable giving is also top of mind for many Canadians as the year wraps up. Golombek notes, “You must make a donation by December 31 to get a donation credit for the current year 2025. However, it’s even better if you have appreciated securities.” Making an in-kind donation of stocks, bonds or mutual funds that have increased in value to a registered charity means “the entire capital gains tax is erased on a donation in kind to a registered charity.” This can be a win-win for both your tax bill and the causes you care about.

Make the most of your RESP withdrawals

When it comes to saving for education, Golombek points out that many focus on contributions to RESPs (Registered Education Savings Plans) but overlook the best way to withdraw funds. “If the students are currently attending school, there’s an opportunity to optimize those withdrawals by taking advantage of all the students’ personal credits, including the basic personal amount, and their tuition credit.” Reviewing a student’s expected income and credits for 2025 can help you withdraw RESP funds in the most tax-efficient way.

First Home Savings Account: Start building contribution room

For those saving for a first home, the FHSA (First Home Savings Account) offers a new opportunity. “You can put in $8,000 for a year, to a maximum of $40,000 during your lifetime. The money is generally tax-deductible when you contribute and, for up to 15 years, grows completely tax sheltered. And if you make a qualifying home purchase within 15 years, the money comes out tax free,” Golombek explains. Even if you don’t make a contribution right away, simply opening an FHSA before December 31 will give you $8,000 of contribution room for 2025, which you can use either this year or in the future.

Apply for a reduction of tax at source

Many Canadians look forward to their tax refund, but Golombek cautions a refund means “you’ve effectively loaned your money to the government interest free.” If you have deductions or credits your employer isn’t aware of, such as RRSP contributions or charitable donations, you can apply to the Canada Revenue Agency (CRA) for a reduction of tax at source. “If the CRA approves that, you can then get a letter that you can give to your employer’s HR department, which will authorize them to reduce the amount of tax they take off from your regular paycheque, essentially getting your tax refund throughout the entire year instead of waiting until the following April.”

Access expert resources

CIBC offers extensive resources to help guide your tax planning. “The CIBC Tax and Estate Planning team has prepared almost 100 publications that are available online,” Golombek shares. Visit cibc.com and look under Smart Advice for the Tax Tips section, where you’ll find the 2025 Tax Toolkit and more.

Partner with professionals

As you consider your year-end tax strategies, remember Golombek’s advice: “You don’t have to do this alone.” Working with a CIBC advisor, alongside a tax expert, lawyer and accountant, can help you navigate the complexities of tax planning and make the most of your financial opportunities.

While there are important steps to take as the year closes, Golombek emphasizes that “tax planning should be a year-round affair.” Staying proactive throughout the year — not just at year-end — can help you maximize your options, avoid last-minute stress, and respond to changes in your financial situation or tax laws as they arise.

Manage Cookie Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.